ERC-4626: analyse performance of individual vaults

In this notebook, we examine a single or handful of handpicked ERC-4626 vaults

Vaults are picked manually by (chain, address) list

We analyse the vault performance by its share price, as reported by ERC-4626 smart contract interface.

We do last three months and historical all-time analyses

We look quantitative finance aspects of the vaults like returns, Sharpe and Sortino numbers

Some notes - Because of how vault metrics, share price and such are collected and interpreted, the results in this notebook contain various inaccuracies. - In this notebook, we use terms Net Asset Value (NAV) and Total Value Locked (TVL) interchangeably.

Usage

This is an open source notebook based on open data - You can edit and remix this notebook yourself

To do your own data research:

Read general instructions how to run the tutorials

See

ERC-4626: scanning vaults' historical price and performanceexample in tutorials first how to buildvault-prices-1h.parquetfile.

For any questions, follow and contact Trading Strategy community.

Setup

Set up notebook rendering output mode

Use static image charts so this notebook is readeable on Github / ReadTheDocs

[8]:

import pandas as pd

from plotly.offline import init_notebook_mode

import plotly.io as pio

from eth_defi.vault.base import VaultSpec

from eth_defi.research.notebook import set_large_plotly_chart_font

pd.options.display.float_format = "{:,.2f}".format

pd.options.display.max_columns = None

pd.options.display.max_rows = None

# Set up Plotly chart output as SVG

image_format = "png"

width = 1400

height = 800

# https://stackoverflow.com/a/52956402/315168

init_notebook_mode()

# https://plotly.com/python/renderers/#overriding-the-default-renderer

pio.renderers.default = image_format

current_renderer = pio.renderers[image_format]

# Have SVGs default pixel with

current_renderer.width = width

current_renderer.height = height

# Set all Plotly charts to use large font sizes for better readability,

# for sharing on mobile

set_large_plotly_chart_font(line_width=5, legend_font_size=16)

pio.templates.default = "custom"

Read and clean raw scanned vault price data

Read the Parquet file produced earlier with price scan

Clean the data if necessary

[9]:

from pathlib import Path

from eth_defi.vault.vaultdb import VaultDatabase

from eth_defi.vault.vaultdb import read_default_vault_prices

from eth_defi.vault.vaultdb import DEFAULT_RAW_PRICE_DATABASE

data_folder = Path("~/.tradingstrategy/vaults").expanduser()

vault_db = VaultDatabase.read()

prices_df = read_default_vault_prices()

print(prices_df.index.max())

print(f"Prices is {DEFAULT_RAW_PRICE_DATABASE}")

print(f"We have {len(vault_db):,} vaults in the database and {len(prices_df):,} price rows.")

2025-12-29 00:55:27

Prices is /Users/moo/.tradingstrategy/vaults/cleaned-vault-prices-1h.parquet

We have 26,576 vaults in the database and 5,953,190 price rows.

Choose vaults to examine

We pick vaults to examine and compare by chain and address tuples

[ ]:

from eth_defi.vault.base import VaultSpec

# Historically troublesome vaults

VAULTS = [

# atvPTmax

# VaultSpec(1, "0xd24e4a98b5fd90ff21a9cc5e2c1254de8084cd81"),

# TODO

VaultSpec(43114, "0x36e2aa296e798ca6262dc5fad5f5660e638d5402"),

# Valamor aUSD http://localhost:5173/trading-view/avalanche/vaults/varlamore-ausd-growth

VaultSpec(43114, "0x3d7b0c3997e48fa3fc96cd057d1fb4e5f891835b"),

# 1337

# VaultSpec(1, "0x94643e86aa5e38ddac6c7791c1297f4e40cd96c1"),

# yearn-v3-USDS-Farmer-USD

# VaultSpec(1, "0x39c0aec5738ed939876245224afc7e09c8480a52"),

# USDC Fluid Lender

# VaultSpec(1, "0x00c8a649c9837523ebb406ceb17a6378ab5c74cf"),

# Harvest USDC Autopilot on IPOR on Base

# https://app.ipor.io/fusion/base/0x0d877dc7c8fa3ad980dfdb18b48ec9f8768359c4/settings

# VaultSpec(8453, "0x0d877Dc7C8Fa3aD980DfDb18B48eC9F8768359C4"),

# IPOR USDC base

# https://app.ipor.io/fusion/base/0x45aa96f0b3188d47a1dafdbefce1db6b37f58216

# VaultSpec(8453, "0x45aa96f0b3188d47a1dafdbefce1db6b37f58216"),

# Summer.fi lazy

# VaultSpec(42161, "0x4f63cfea7458221cb3a0eee2f31f7424ad34bb58"),

# gTRADE (Gains) on Polygon

# https://app.ipor.io/fusion/base/0x45aa96f0b3188d47a1dafdbefce1db6b37f58216

# VaultSpec(137, "0x29019fe2e72e8d4d2118e8d0318bef389ffe2c81"),

# Gains on ARbitrum

# 42161-0xd85e038593d7a098614721eae955ec2022b9b91b

# VaultSpec(42161, "0xd85e038593d7a098614721eae955ec2022b9b91b"),

# gUSD on Arbitrum

# VaultSpec(42161, "0xd3443ee1e91af28e5fb858fbd0d72a63ba8046e0"),

# Peapods arbitrum

# VaultSpec(42161, "0xc2810eb57526df869049fbf4c541791a3255d24c"),

# Degen pool USDC 42161-0x20a1012b79e8f3ca3f802533c07934ef97398da

# VaultSpec(42161, "0x20a1012b79e8f3ca3f802533c07934ef97398da7"),

# Fluegel DAO

# 8453-0x277a3c57f3236a7d4548576074d7c3d7046eb26c

# https://fluegelcoin.com/dashboard

# VaultSpec(8453, "0x277a3c57f3236a7d4548576074d7c3d7046eb26c"),

# Plutus hedge on Arbitrum

# VaultSpec(42161, "0x58BfC95a864e18E8F3041D2FCD3418f48393fE6A"),

# crvUSD IBTC

# VaultSpec(42161, "0xe296ee7f83d1d95b3f7827ff1d08fe1e4cf09d8d"),

# D2 Hype on Arbitrum

# VaultSpec(42161, "0x75288264FDFEA8ce68e6D852696aB1cE2f3E5004"),

# Fluid on Ethereum

# VaultSpec(1, "0x00c8a649c9837523ebb406ceb17a6378ab5c74cf"),

# Upshift gamma

# VaultSpec(1, "0x998d7b14c123c1982404562b68eddb057b0477cb"),

]

Period selection

Choose the period we want to examine

Comment out the trim operation if you want to examine the latest data

[11]:

last_sample_at = prices_df.index.max()

three_months_ago = last_sample_at - pd.DateOffset(months=3)

PERIOD = [

three_months_ago,

last_sample_at,

]

print(f"Trimming price data to period from {PERIOD[0]} to {PERIOD[1]}.")

mask = (prices_df.index >= PERIOD[0]) & (prices_df.index <= PERIOD[1])

prices_df = prices_df[mask]

print(f"Trimmed period contains {len(prices_df):,} price rows.")

prices_df = prices_df.sort_index()

display(prices_df.tail(2))

Trimming price data to period from 2025-09-29 00:55:27 to 2025-12-29 00:55:27.

Trimmed period contains 969,491 price rows.

| id | chain | address | block_number | share_price | total_assets | total_supply | performance_fee | management_fee | errors | name | event_count | protocol | raw_share_price | returns_1h | avg_assets_by_vault | dynamic_tvl_threshold | tvl_filtering_mask | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| timestamp | ||||||||||||||||||

| 2025-12-29 00:55:27 | 10-0x6926b434cce9b5b7966ae1bfeef6d0a7dcf3a8bb | 10 | 0x6926b434cce9b5b7966ae1bfeef6d0a7dcf3a8bb | 145685475 | 1.09 | 1,882,561.42 | 1,727,893.56 | NaN | NaN | exactly USDC | 226488 | <protocol not yet identified> | 1.09 | 0.00 | 4,566,831.10 | 91,336.62 | False | |

| 2025-12-29 00:55:27 | 10-0x035c93db04e5aaea54e6cd0261c492a3e0638b37 | 10 | 0x035c93db04e5aaea54e6cd0261c492a3e0638b37 | 145685475 | 1.21 | 49,705.69 | 40,986.76 | NaN | NaN | Static Aave Optimism USDT | 33407 | Superform | 1.21 | 0.00 | 40,618.50 | 812.37 | False |

Examine data

Examine metadata

[12]:

examined_vault_spec = VAULTS[0]

examined_id = f"{examined_vault_spec.chain_id}-{examined_vault_spec.vault_address}"

vault_metadata = vault_db.rows[examined_vault_spec]

display(vault_metadata)

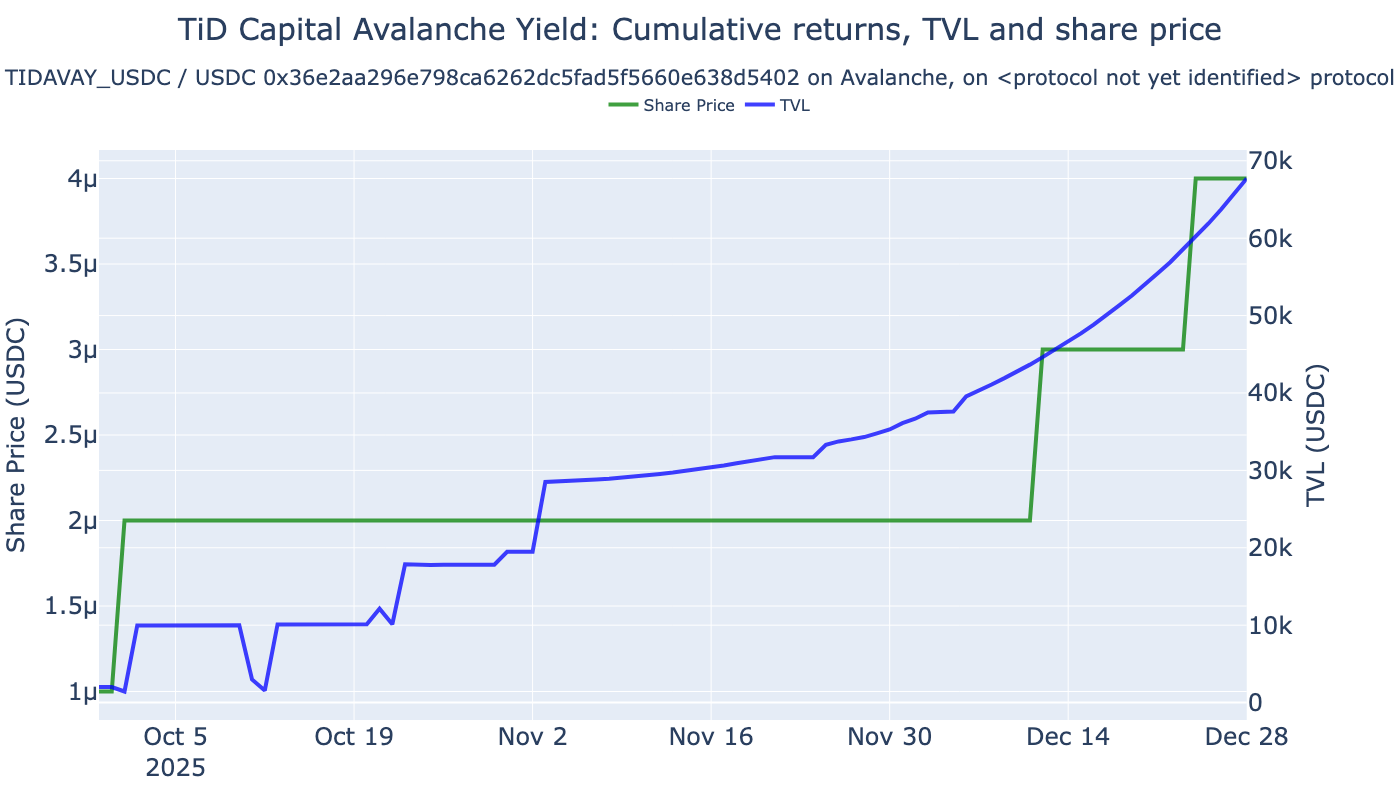

{'Symbol': 'TIDAVAY_USDC',

'Name': 'TiD Capital Avalanche Yield',

'Address': '0x36e2aa296e798ca6262dc5fad5f5660e638d5402',

'Denomination': 'USDC',

'Share token': 'TIDAVAY_USDC',

'NAV': Decimal('67801.754191'),

'Protocol': '<protocol not yet identified>',

'Mgmt fee': None,

'Perf fee': None,

'Deposit fee': None,

'Withdraw fee': None,

'Shares': Decimal('14232270910.974665'),

'First seen': datetime.datetime(2025, 9, 27, 7, 51, 43),

'Features': '',

'Link': 'https://routescan.io/address/0x36E2AA296E798Ca6262DC5Fad5F5660e638d5402',

'_detection_data': ERC4262VaultDetection(chain=43114, address='0x36e2aa296e798ca6262dc5fad5f5660e638d5402', first_seen_at_block=69371655, first_seen_at=datetime.datetime(2025, 9, 27, 7, 51, 43), features=set(), updated_at=datetime.datetime(2025, 12, 29, 0, 50, 4, 453740), deposit_count=15, redeem_count=13),

'_denomination_token': {'name': 'USD Coin',

'symbol': 'USDC',

'total_supply': 569693925223775,

'decimals': 6,

'extra_data': {'cached': True},

'address': '0xB97EF9Ef8734C71904D8002F8b6Bc66Dd9c48a6E',

'chain': 43114},

'_share_token': {'name': 'TiD Capital Avalanche Yield',

'symbol': 'TIDAVAY_USDC',

'total_supply': 14232270910974665,

'decimals': 6,

'extra_data': {'cached': True},

'address': '0x36E2AA296E798Ca6262DC5Fad5F5660e638d5402',

'chain': 43114},

'_fees': FeeData(fee_mode=None, management=None, performance=None, deposit=None, withdraw=None),

'_flags': set(),

'_lockup': None}

Vault charts and performance tearsheets

Examine vault metrics and charts

[14]:

from eth_defi.research.vault_metrics import analyse_vault, format_ffn_performance_stats

from eth_defi.chain import get_chain_name

from IPython.display import display, HTML

for vault_spec in VAULTS:

vault_report = analyse_vault(

vault_db=vault_db,

prices_df=prices_df,

spec=vault_spec,

chart_frequency="daily",

)

chain_name = get_chain_name(vault_spec.chain_id)

vault_name = vault_report.vault_metadata["Name"]

print(f"Analysing vault {vault_name} ({chain_name}): {vault_spec.as_string_id()}")

display(HTML(f"<h2>Vault {vault_name} ({chain_name}): {vault_spec.vault_address})</h2><br>"))

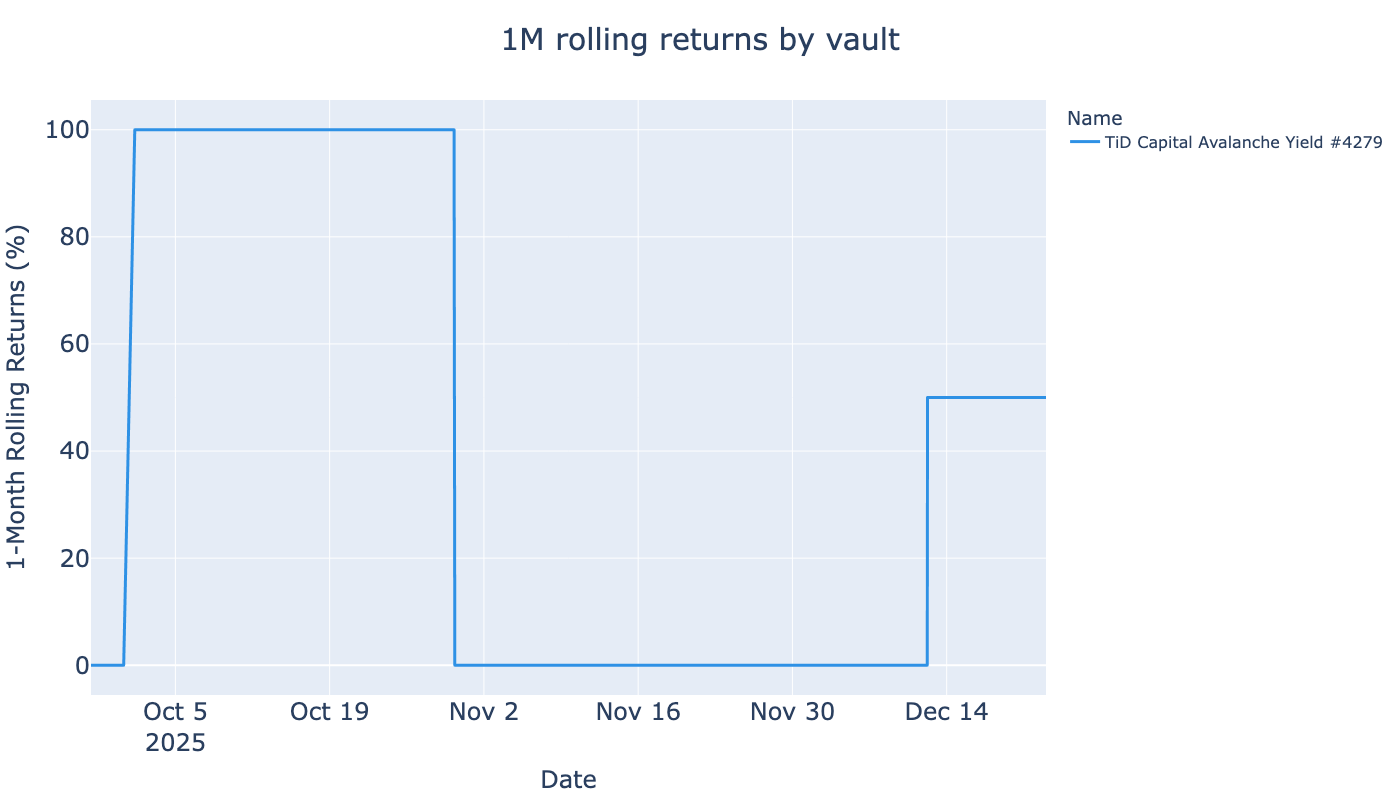

# Display returns figur

returns_chart_fig = vault_report.rolling_returns_chart

returns_chart_fig.show()

# Check raw montly share price numbers for each vault

hourly_price_df = vault_report.hourly_df

last_price_at = hourly_price_df.index[-1]

last_price = hourly_price_df["share_price"].asof(last_price_at)

last_block = hourly_price_df["block_number"].asof(last_price_at)

month_ago = last_price_at - pd.DateOffset(months=1)

month_ago_price = hourly_price_df["share_price"].asof(month_ago)

month_ago_block = hourly_price_df["block_number"].asof(month_ago)

if not pd.isna(month_ago_price):

print(f"Vault {vault_spec.chain_id}-{vault_spec.vault_address}: no price data for month ago {month_ago} found, last price at {last_price_at} is {last_price}")

continue

data = {

"Vault": f"{vault_name} ({chain_name})",

"Last price at": last_price_at,

"Last price": last_price,

"Block last price": f"{month_ago_block:,}",

"Month ago": month_ago,

"Block month ago": f"{month_ago_block:,}",

"Month ago price": month_ago_price,

"Monthly change %": (last_price - month_ago_price) / month_ago_price * 100,

}

df = pd.Series(data)

display(df)

# Display FFN stats

performance_stats = vault_report.performance_stats

if performance_stats is not None:

stats_df = format_ffn_performance_stats(performance_stats)

# display(stats_df)

display(HTML(stats_df.to_frame(name='Value').to_html(float_format='{:,.2f}'.format, index=True)))

else:

print(f"Vault {vault_spec.chain_id}-{vault_spec.vault_address}: performance metrics not available, is quantstats library installed?")

Share price movement: 0.0000 2025-09-29 15:00:00 -> 0.0000 2025-12-28 23:00:00

Analysing vault TiD Capital Avalanche Yield (Avalanche): 43114-0x36e2aa296e798ca6262dc5fad5f5660e638d5402

Vault TiD Capital Avalanche Yield (Avalanche): 0x36e2aa296e798ca6262dc5fad5f5660e638d5402)

Vault 43114-0x36e2aa296e798ca6262dc5fad5f5660e638d5402: no price data for month ago 2025-11-28 23:00:00 found, last price at 2025-12-28 23:00:00 is 4e-06

---------------------------------------------------------------------------

AssertionError Traceback (most recent call last)

Cell In[14], line 8

4 from IPython.display import display, HTML

6 for vault_spec in VAULTS:

----> 8 vault_report = analyse_vault(

9 vault_db=vault_db,

10 prices_df=prices_df,

11 spec=vault_spec,

12 chart_frequency="daily",

13 )

15 chain_name = get_chain_name(vault_spec.chain_id)

16 vault_name = vault_report.vault_metadata["Name"]

File ~/code/trade-executor/deps/web3-ethereum-defi/eth_defi/research/vault_metrics.py:1268, in analyse_vault(vault_db, prices_df, spec, returns_col, logger, chart_frequency)

1266 vault_metadata = vault_db.get(spec)

1267 if vault_metadata is None:

-> 1268 assert vault_metadata, f"Vault with id {spec} not found in vault database"

1270 chain_name = get_chain_name(spec.chain_id)

1271 name = vault_metadata["Name"]

AssertionError: Vault with id VaultSpec(chain_id=43114, vault_address='0x3d7b0c3997e48fa3fc96cd057d1fb4e5f891835b1') not found in vault database

Rolling returns comparison

Show rolling returns of all picked vaults

[ ]:

from eth_defi.research.rolling_returns import calculate_rolling_returns, visualise_rolling_returns

interesting_vaults = [spec.as_string_id() for spec in VAULTS]

rolling_returns_df = calculate_rolling_returns(

prices_df,

interesting_vaults=interesting_vaults,

clip_up=100,

)

display(rolling_returns_df.head(3))

fig = visualise_rolling_returns(rolling_returns_df)

fig.show()

| id | timestamp | chain | address | block_number | share_price | total_assets | total_supply | performance_fee | management_fee | errors | name | event_count | protocol | raw_share_price | returns_1h | avg_assets_by_vault | dynamic_tvl_threshold | tvl_filtering_mask | rolling_1m_returns | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 43114-0x36e2aa296e798ca6262dc5fad5f5660e638d5402 | 2025-09-27 08:10:55 | 43114 | 0x36e2aa296e798ca6262dc5fad5f5660e638d5402 | 69372297 | 0.00 | 2,000.00 | 2,000,000,000.00 | NaN | NaN | TiD Capital Avalanche Yield #4279 | 28 | <protocol not yet identified> | 0.00 | NaN | 23,645.82 | 472.92 | False | 0.00 | |

| 1 | 43114-0x36e2aa296e798ca6262dc5fad5f5660e638d5402 | 2025-09-27 09:02:48 | 43114 | 0x36e2aa296e798ca6262dc5fad5f5660e638d5402 | 69374097 | 0.00 | 2,000.02 | 2,000,000,000.00 | NaN | NaN | TiD Capital Avalanche Yield #4279 | 28 | <protocol not yet identified> | 0.00 | 0.00 | 23,645.82 | 472.92 | False | 0.00 | |

| 2 | 43114-0x36e2aa296e798ca6262dc5fad5f5660e638d5402 | 2025-09-27 09:51:12 | 43114 | 0x36e2aa296e798ca6262dc5fad5f5660e638d5402 | 69375897 | 0.00 | 2,000.02 | 2,000,000,000.00 | NaN | NaN | TiD Capital Avalanche Yield #4279 | 28 | <protocol not yet identified> | 0.00 | 0.00 | 23,645.82 | 472.92 | False | 0.00 |

Raw vault data

Examine raw data of a single vault

Find abnormal return rows

[ ]:

# Fluegel DAO

# 8453-0x277a3c57f3236a7d4548576074d7c3d7046eb26c

# https://fluegelcoin.com/dashboard

vault_spec = VaultSpec(8453, "0x277a3c57f3236a7d4548576074d7c3d7046eb26c")

df = prices_df[prices_df["id"] == vault_spec.as_string_id()]

# 10% claimed hourly returns

mask = df["returns_1h"].abs() > 0.10

expanded_mask = (mask | mask.shift(1) | mask.shift(-1)).fillna(False)

df = df[expanded_mask] # Filter out rows with small returns

display(df.head(10))

| id | chain | address | block_number | share_price | total_assets | total_supply | performance_fee | management_fee | errors | name | event_count | protocol | raw_share_price | returns_1h | avg_assets_by_vault | dynamic_tvl_threshold | tvl_filtering_mask | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| timestamp | ||||||||||||||||||

| 2025-09-24 08:36:07 | 8453-0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 8453 | 0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 35956810 | 2.04 | 661,538.44 | 323,616.44 | NaN | NaN | Fluegel DAO (Base) #248 | 555 | <protocol not yet identified> | 2.04 | -0.00 | 603,195.56 | 12,063.91 | False | |

| 2025-09-24 10:36:07 | 8453-0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 8453 | 0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 35960410 | 1.82 | 588,709.80 | 323,616.44 | NaN | NaN | Fluegel DAO (Base) #248 | 555 | <protocol not yet identified> | 1.82 | -0.11 | 603,195.56 | 12,063.91 | False | |

| 2025-09-24 11:36:07 | 8453-0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 8453 | 0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 35962210 | 2.07 | 669,008.32 | 323,616.44 | NaN | NaN | Fluegel DAO (Base) #248 | 555 | <protocol not yet identified> | 2.07 | 0.14 | 603,195.56 | 12,063.91 | False | |

| 2025-09-24 13:36:07 | 8453-0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 8453 | 0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 35965810 | 2.06 | 667,852.18 | 323,616.44 | NaN | NaN | Fluegel DAO (Base) #248 | 555 | <protocol not yet identified> | 2.06 | -0.00 | 603,195.56 | 12,063.91 | False | |

| 2025-10-01 17:36:07 | 8453-0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 8453 | 0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 36275410 | 2.25 | 727,138.15 | 323,616.44 | NaN | NaN | Fluegel DAO (Base) #248 | 555 | <protocol not yet identified> | 2.25 | -0.01 | 603,195.56 | 12,063.91 | False | |

| 2025-10-01 18:36:07 | 8453-0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 8453 | 0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 36277210 | 1.99 | 644,306.79 | 323,616.44 | NaN | NaN | Fluegel DAO (Base) #248 | 555 | <protocol not yet identified> | 1.99 | -0.11 | 603,195.56 | 12,063.91 | False | |

| 2025-10-01 19:36:07 | 8453-0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 8453 | 0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 36279010 | 2.25 | 728,047.48 | 323,616.44 | NaN | NaN | Fluegel DAO (Base) #248 | 555 | <protocol not yet identified> | 2.25 | 0.13 | 603,195.56 | 12,063.91 | False | |

| 2025-10-01 20:36:07 | 8453-0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 8453 | 0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 36280810 | 2.24 | 725,813.95 | 323,616.44 | NaN | NaN | Fluegel DAO (Base) #248 | 555 | <protocol not yet identified> | 2.24 | -0.00 | 603,195.56 | 12,063.91 | False | |

| 2025-10-01 22:36:07 | 8453-0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 8453 | 0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 36284410 | 2.27 | 733,985.44 | 323,616.44 | NaN | NaN | Fluegel DAO (Base) #248 | 555 | <protocol not yet identified> | 2.27 | 0.00 | 603,195.56 | 12,063.91 | False | |

| 2025-10-01 23:36:07 | 8453-0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 8453 | 0x277a3c57f3236a7d4548576074d7c3d7046eb26c | 36286210 | 2.03 | 655,645.90 | 323,616.44 | NaN | NaN | Fluegel DAO (Base) #248 | 555 | <protocol not yet identified> | 2.03 | -0.11 | 603,195.56 | 12,063.91 | False |