Derive historical open interest and funding rate

Derive is a decentralised options and perpetual futures exchange built on its own OP Stack L2 chain (Derive Chain, chain ID 957). This notebook visualises historical open interest and funding rate data for BTC and ETH perpetual contracts.

Open interest measures the total outstanding perpetual positions (in base currency units, e.g. BTC or ETH). It is read from on-chain state via Multicall3.

Funding rate is the hourly rate paid between longs and shorts to keep the perpetual price anchored to the index price. It is fetched from Derive’s REST API.

For full details on the Derive integration, data sources, API quirks and scan scripts, see README-derive.md.

Populating the DuckDB database

This notebook reads from a local DuckDB database at ~/.tradingstrategy/derive/funding-rates.duckdb. You must populate it before running the notebook by executing the two scan scripts:

1. Scan funding rates (hourly snapshots from Derive REST API, ~2-3 min for full history):

poetry run python scripts/derive/scan-funding-rates.py

2. Scan open interest (daily on-chain snapshots via Multicall3, ~20 min for full backfill):

poetry run python scripts/derive/scan-open-interest.py

Both scripts are incremental — subsequent runs only fetch new data since the last sync. You can limit the sync to specific instruments with INSTRUMENTS=ETH-PERP,BTC-PERP or control the database path with DB_PATH. See README-derive.md for all environment variables and performance benchmarks.

Running this notebook

Run from the command line:

poetry run jupyter execute docs/source/tutorials/derive-open-interest-funding-rate.ipynb --inplace --timeout=900

Or open in Visual Studio Code / JupyterLab.

[1]:

# Set up static PNG chart output

from eth_defi.research.notebook import setup_charting_and_output, OutputMode, set_large_plotly_chart_font

setup_charting_and_output(OutputMode.static, image_format="png", width=1500, height=800, increase_font_size=False)

set_large_plotly_chart_font()

import datetime

import pandas as pd

import plotly.graph_objects as go

from plotly.subplots import make_subplots

from eth_defi.derive.historical import DeriveFundingRateDatabase

Load data from local DuckDB

[2]:

db = DeriveFundingRateDatabase()

start_time = datetime.datetime(2025, 1, 1)

# Fetch open interest DataFrames (columns: timestamp, instrument, open_interest, perp_price, index_price)

btc_oi_df = db.get_open_interest_dataframe("BTC-PERP", start_time=start_time)

eth_oi_df = db.get_open_interest_dataframe("ETH-PERP", start_time=start_time)

# Fetch funding rate DataFrames (columns: timestamp, instrument, funding_rate)

btc_fr_df = db.get_funding_rates_dataframe("BTC-PERP", start_time=start_time)

eth_fr_df = db.get_funding_rates_dataframe("ETH-PERP", start_time=start_time)

db.close()

# Compute OI in USD terms using index price

btc_oi_df["oi_usd"] = btc_oi_df["open_interest"].astype(float) * btc_oi_df["index_price"].astype(float)

eth_oi_df["oi_usd"] = eth_oi_df["open_interest"].astype(float) * eth_oi_df["index_price"].astype(float)

# Resample hourly funding rates to daily mean for cleaner charts

btc_fr_daily = btc_fr_df.set_index("timestamp")["funding_rate"].resample("1D").mean().reset_index()

eth_fr_daily = eth_fr_df.set_index("timestamp")["funding_rate"].resample("1D").mean().reset_index()

summary = pd.DataFrame({

"Instrument": ["BTC-PERP", "ETH-PERP"],

"OI rows": [len(btc_oi_df), len(eth_oi_df)],

"Funding rate rows": [len(btc_fr_df), len(eth_fr_df)],

"OI date range": [

f"{btc_oi_df['timestamp'].min()} - {btc_oi_df['timestamp'].max()}",

f"{eth_oi_df['timestamp'].min()} - {eth_oi_df['timestamp'].max()}",

],

})

display(summary)

| Instrument | OI rows | Funding rate rows | OI date range | |

|---|---|---|---|---|

| 0 | BTC-PERP | 10630 | 10636 | 2025-01-01 00:00:01 - 2026-03-19 21:00:01 |

| 1 | ETH-PERP | 10630 | 10637 | 2025-01-01 00:00:01 - 2026-03-19 21:00:01 |

Summary metrics

[3]:

def compute_metrics(fr_df: pd.DataFrame, oi_df: pd.DataFrame, name: str) -> dict:

"""Compute funding rate and OI metrics for one instrument."""

fr = fr_df["funding_rate"].astype(float)

hours_positive = int((fr > 0).sum())

hours_negative = int((fr < 0).sum())

total_hours = len(fr)

mean_hourly = fr.mean()

oi_usd = oi_df["oi_usd"]

return {

"Instrument": name,

"Hours positive": f"{hours_positive:,}",

"Hours negative": f"{hours_negative:,}",

"% hours positive": f"{100 * hours_positive / total_hours:.1f}%",

"Mean hourly rate": f"{mean_hourly:.8f}",

"Annualised rate": f"{mean_hourly * 8760:.2%}",

"Max hourly rate": f"{fr.max():.8f}",

"Min hourly rate": f"{fr.min():.8f}",

"Cumulative funding": f"{fr.sum():.4f}",

"Current OI (USD)": f"${oi_usd.iloc[-1]:,.0f}",

"Peak OI (USD)": f"${oi_usd.max():,.0f}",

"Mean OI (USD)": f"${oi_usd.mean():,.0f}",

}

metrics = pd.DataFrame([

compute_metrics(btc_fr_df, btc_oi_df, "BTC-PERP"),

compute_metrics(eth_fr_df, eth_oi_df, "ETH-PERP"),

]).set_index("Instrument").T

metrics.index.name = None

display(metrics)

| Instrument | BTC-PERP | ETH-PERP |

|---|---|---|

| Hours positive | 8,718 | 8,987 |

| Hours negative | 1,918 | 1,650 |

| % hours positive | 82.0% | 84.5% |

| Mean hourly rate | 0.00001250 | 0.00001131 |

| Annualised rate | 10.95% | 9.91% |

| Max hourly rate | 0.00045662 | 0.00078069 |

| Min hourly rate | -0.00021506 | -0.00034533 |

| Cumulative funding | 0.1330 | 0.1203 |

| Current OI (USD) | $25,622,330 | $7,181,877 |

| Peak OI (USD) | $26,845,258 | $22,495,469 |

| Mean OI (USD) | $11,685,941 | $8,303,178 |

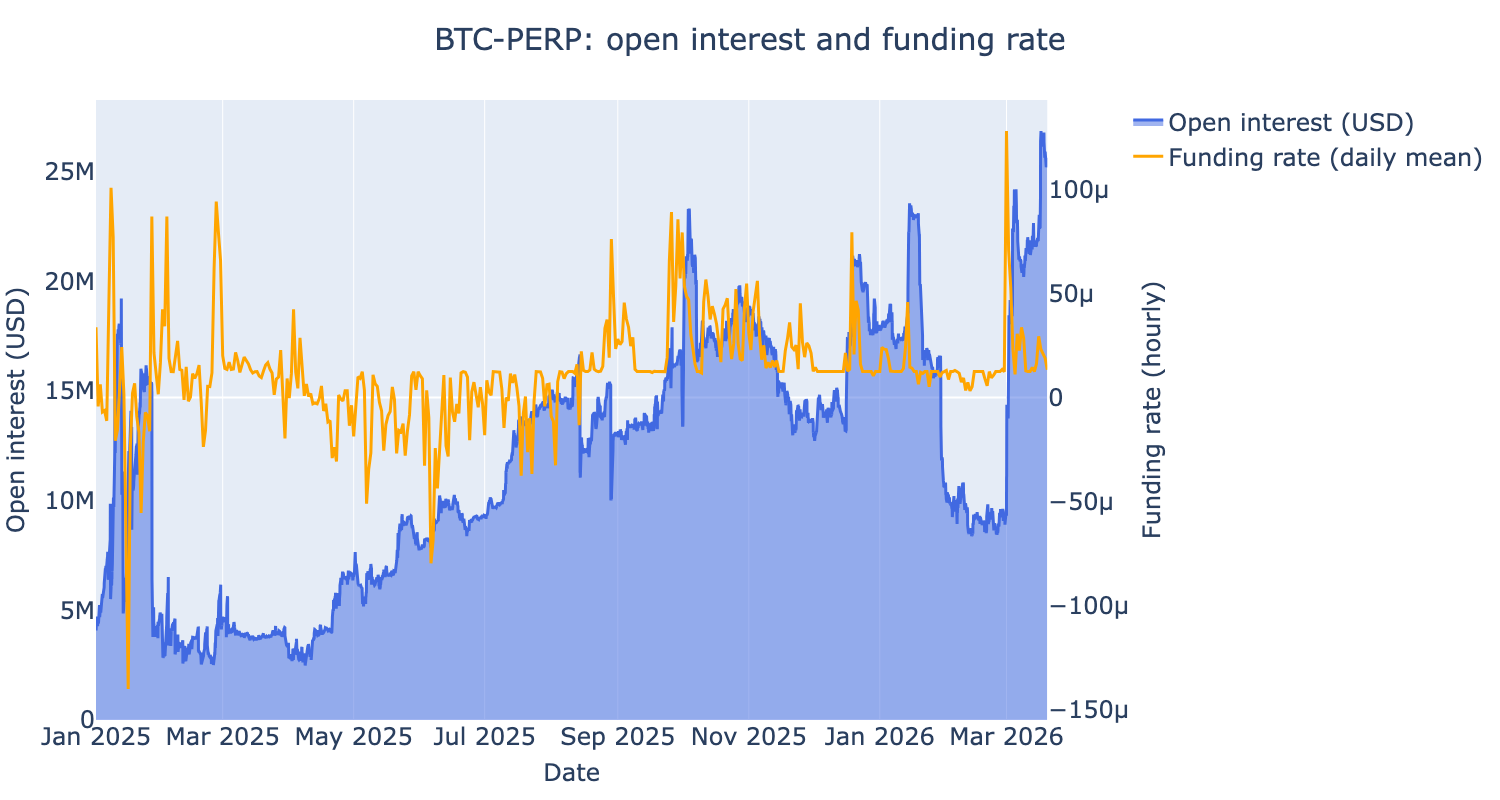

BTC open interest and funding rate

[4]:

fig = make_subplots(specs=[[{"secondary_y": True}]])

# Open interest in USD on left y-axis

fig.add_trace(

go.Scatter(

x=btc_oi_df["timestamp"],

y=btc_oi_df["oi_usd"],

name="Open interest (USD)",

fill="tozeroy",

line=dict(color="royalblue"),

),

secondary_y=False,

)

# Daily mean funding rate on right y-axis

fig.add_trace(

go.Scatter(

x=btc_fr_daily["timestamp"],

y=btc_fr_daily["funding_rate"].astype(float),

name="Funding rate (daily mean)",

line=dict(color="orange"),

),

secondary_y=True,

)

fig.update_layout(title="BTC-PERP: open interest and funding rate", height=600)

fig.update_yaxes(title_text="Open interest (USD)", secondary_y=False, showgrid=False)

fig.update_yaxes(title_text="Funding rate (hourly)", secondary_y=True, showgrid=False)

fig.update_xaxes(title_text="Date")

fig.show()

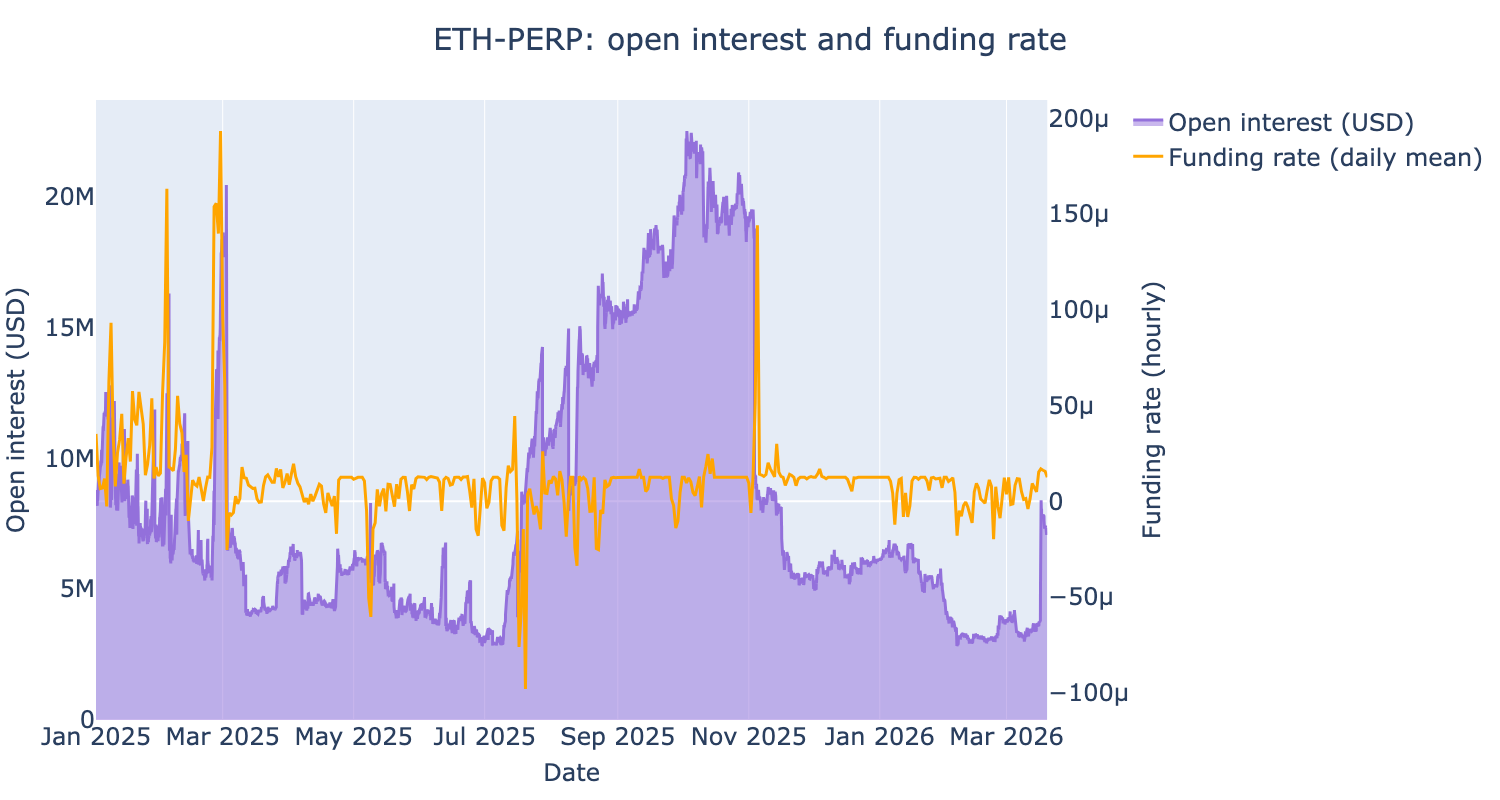

ETH open interest and funding rate

[5]:

fig = make_subplots(specs=[[{"secondary_y": True}]])

# Open interest in USD on left y-axis

fig.add_trace(

go.Scatter(

x=eth_oi_df["timestamp"],

y=eth_oi_df["oi_usd"],

name="Open interest (USD)",

fill="tozeroy",

line=dict(color="mediumpurple"),

),

secondary_y=False,

)

# Daily mean funding rate on right y-axis

fig.add_trace(

go.Scatter(

x=eth_fr_daily["timestamp"],

y=eth_fr_daily["funding_rate"].astype(float),

name="Funding rate (daily mean)",

line=dict(color="orange"),

),

secondary_y=True,

)

fig.update_layout(title="ETH-PERP: open interest and funding rate", height=600)

fig.update_yaxes(title_text="Open interest (USD)", secondary_y=False, showgrid=False)

fig.update_yaxes(title_text="Funding rate (hourly)", secondary_y=True, showgrid=False)

fig.update_xaxes(title_text="Date")

fig.show()